Coal Tax Policy

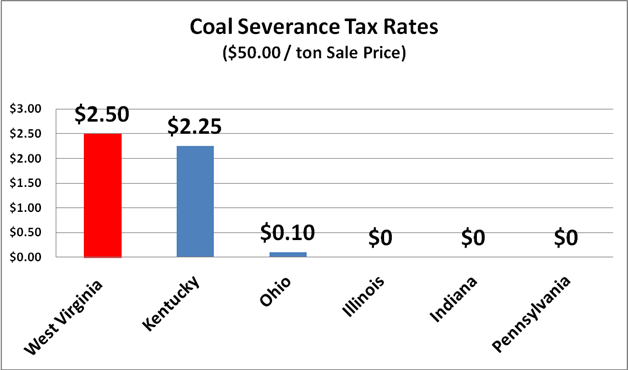

The glaring obstacle serving to impede West Virginia’s competitiveness and market share is the State’s unparalleled level of severance tax imposed on coal tonnage.

Make no mistake about it, West Virginia’s severance tax rate of 5% has no parallel in any other state. Consequently, coal from neighboring states squeezes out West Virginia coal from regional, dwindling markets.

Reducing the sate severance rate from 5% to 2% is a fair and reasonable proposition. Any and all fiscal gains secured from lower taxation will absolutely not go to producers but instead will be realized at the coal-fired power plant where the coal is utilized.

Lowering the cost and tax burden on coal-fired generation will also translate into the electricity produced to elevate on the order of economic dispatch from utilities to its consumer base resulting in higher volumes of power to flow at reduced costs. This will not only sustain the overall health of the coal industry but additionally preserve its high paying job base and simultaneously reduce the cost of household and industrial power for all state residents and businesses.

We respectfully request the Legislature to take immediate steps to lower the unprecedented five percent (5%) severance tax on active “steam” coal production.

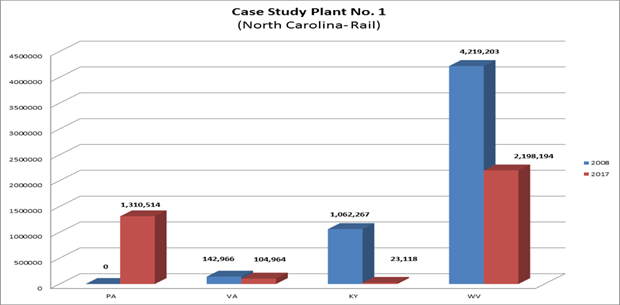

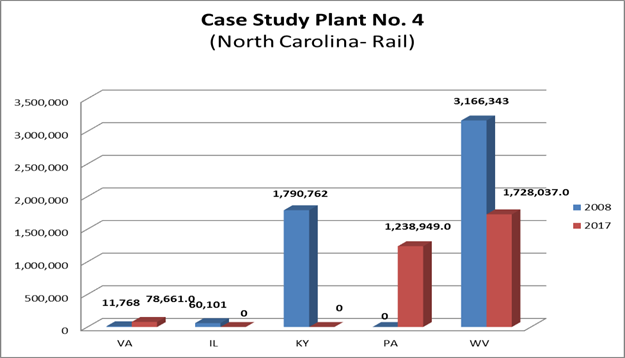

Case Study Plant #1 is in North Carolina and received shipments of coal via “rail”. The following graph shows that West Virginia coal was reduced by half from CY 2008 to CY 2018 or 4,219,203 tons to 2,198,194 tons, while coal from PA (which has a 0% severance rate) captured one third of the plant’s burn or 1,310,514 tons in FY 2017.

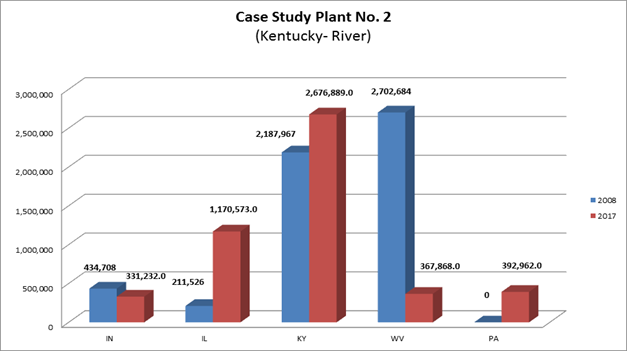

The Second Case Study Plant #2, involves a Kentucky utility that is served by “river”. West Virginia’s share of this market dropped by over 700% over the Study period (2018-2017) from a high of 2,702,684 tons down to 367,868 tons. During the same period, coal from the IL basin grew by over 500 % from 311,526 to 1,170,573; KY’s share went from 2,187,967 tons to 2,676,889 tons and the State of PA added 392,962 of “new” coal supply.

Conclusion

It is our belief that lowering the severance tax rate on West Virginia coal will allow more coal tobe purchased by utilities within our marketing region and will help position West Virginia coalmining operations to capitalize on future growth in electricity demand. Reducing the state severance tax rate from 5% to 2% is a fair and reasonable proposition. Any and all fiscal gains secured from lower taxation will absolutely not go to producers but instead will be realized at the coal-fired [power plant where the coal is utilized.

Extending the Economic Opportunity Tax Credit (EOTC) to our natural resource industry will help offset the capitol necessary to open or expand new mining operations and help influence a greater share of investment dollars to projects in West Virginia.

Lowering the cost and tax burden on coal-fired generation will also translate into the electricity produced to elevate on the order of economic dispatch from utilities to its consumer base resulting in higher volumes of power to flow at reduced costs. This will not only sustain the overall health of the coal industry but additionally preserve its high paying job base and simultaneously reduce the cost of household and industrial power for all state residents and businesses.

We have that opportunity today and the time to act is now! We must do whatever is humanly possible on the state level to protect the tens of thousands of West Virginians who work in and around our coal operations including COALMINERS, RAILROADERS, CONTRACTORS, TRUCKERS, BARGE WORKERS, RIVER PILOTS, MINE VENDORS, SUPPLIERS, POWER PLANT OPERATORS and UTILITY WORKERS.

Economic Opportunity Tax Credit:

The Economic Opportunity Tax Credit was enacted in 2002 and currently applies to investments by taxpayers in certain industries, such as manufacturing, power generation, natural gas processing, warehousing, goods distribution and tourism. The Economic Opportunity Tax Credit is used to offset B&O taxes, CNIT, business franchise tax and certain personal income taxes. By extending the tax to coal mining operations, it would attract greater investment opportunities in West Virginia by multi-state mining companies looking to expand their coal output effectively resulting in equipment purchases and greater employment. Two basic changes to the current program are needed to allow it to be used to promote investment in the coal industry. First, coal production would need to be added to list of favored industries who can claim the EOTC. Second, the EOTC would need to be amended to allow the credit to be used to offset severance tax liability.